Medicare Part A, B, C, and D. The Differences in Each Plan

Where to Go to Get Started and What You Will Need

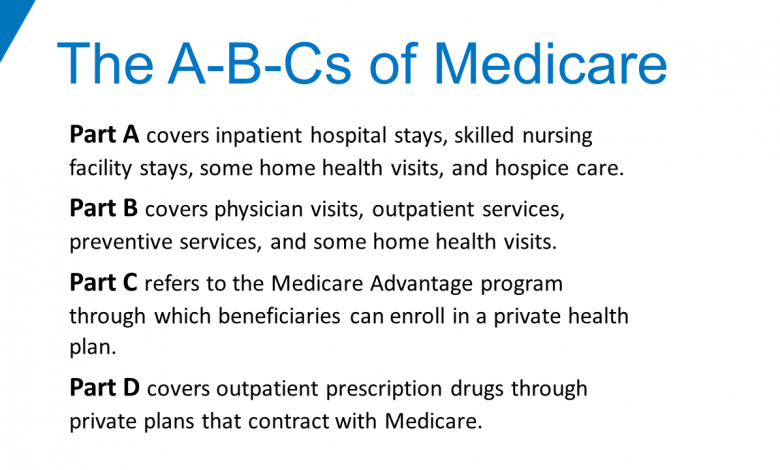

There are different parts of Medicare, and you need to know them and their elaborations in order to know the best one to choose from. Currently, there are four parts of Medicare you should be aware of, below we will go through each part to help you determine which Medicare Part is best for your needs. You will want to go through all these details and make sure you understand before you choose the coverage matching your health needs. Currently, there is original Medicare, which you will get directly from the federal government. Medicare Part A is health insurance that covers hospital insurance. This insurance covers the first 60 days of a hospital visit for room and board with a deductible. Medicare Part A also covers some home health services, nursing care, and hospice care. Medicare Part A does not cover private hospital rooms unless it is medically necessary or a personal private nurse. If individuals need to be hospitalized longer than the 60 days supplemental insurance may be needed to cover the rest of the costs.

Qualifying For Part A

In order to qualify for Medicare Part A there are a few ways to qualify which are if an individual is at least 65 years old, be collecting benefits from social security or railroad retirement, received Medicare through government employment, and finally if someone has a permanent disability or specific diseases. The initial enrollment period to apply is 3 months before an individuals 65th birthday and 3 months after an individual’s 65th birthday. This is very beneficial for senior citizens or people with disabilities that are in need of hospital care.

Medicare Part B

Medicare Part B is a portion of the original Medicare plan that covers medical service and all of the medical supplies that are needed to help treat the condition the patient comes in for. In addition, by covering those portions of medical care Medicare Part B also covers rehabilitation services that a doctor may order for a patient. This is known as medical insurance, and it is only applicable when you pay a monthly premium in order to have this access. Some common services you will access include x-ray, laboratory, outpatient, preventative care, checkups, access to equipment and ambulance services. Moreover, this plan also covers preventative health care services for individuals who may need them. For example, it covers flu shots, hepatitis shots, multiple health screening services.

Qualifying For Part B

The qualifications for Medicare Part B are exactly the same as Part A revolving around being aged 65 or older or suffering from specific disabilities or diseases. Most Individuals do have to pay a monthly premium, unlike Part A which is usually premium free, unless an individual makes too much money they will monthly premium for Part A also. The averaged monthly premium cost for Medicare Part B is usually between $130-$134 per month if individuals making less than $85,000 per year in the current year of 2018. Part B does have deductibles which are usually around $183 per year along with 20% coinsurance that individuals are responsible for paying. These co-pays help protect individuals from doctors charging individuals more than the Medicare-approved amount for the services rendered.

Medicare Part C

Medicare Part C is usually called Medicare Advantage which is an alternative plan to the Medicare Plans A and B which is considered the original Medicare. Medicare Part C is offered by private insurance companies that have been approved by Medicare. Medicare Advantage covers everything both Part A and Part B covers and usually has added coverage for prescription drugs depending on the chosen plan. There are also plans that provide health insurance covering dental, eye, and hearing services.

Different From Part A and B

Medicare Part C does come with a monthly premium that plan holders do have to pay for benefits of Medicare Advantage. Moreover, this is a limit on how much insurance companies can charge when offering Medicare Advantage plans; this can bring a sigh of relief for many choosing to take advantage of Medicare Advantage plans over original Medicare Plans. Continuing on a lot of plans also charge a yearly deductible and some co-pays when choosing medical services. Lastly, Medical Advantage Plans do have different coinsurance prices and percentages that share the cost of medical services between the insurance provider and the plan holder. Medicare Advantage plans are great Medicare Plans that help users get all of their medical needs in one large plan.

Medicare Part D

Medicare Part D is a plan for prescription drugs that are also known as Medicare prescription drug benefit. This plan is offered by the United State Government for individuals looking for assistance in paying for prescription drugs costs. The average monthly cost for Medicare Part D is around $34 a month in the current year of 2018. It is very important to remember that the Medicare prescription drug benefit is an optional plan and if not chosen when first applying for Medicare a late enrollment fee will be charged if an individual wants to take advantage of the prescription drug benefits.

How Medicare part D Helps

Another important thing to remember is that original Medicare does not cover the cost of prescription drugs, so to have some assistance this plan might be needed. The only two ways to receive benefits from Medicare prescription drug benefit. The first is by applying for the original Medicare Part D plan and the second is by choosing a Medicare Advantage Plan that has prescription drug benefits built into the plan. Individuals are eligible to take advantage of this plan as soon as they are eligible to receive benefits from Part A and Part B. Concluding this is a plan that can be very beneficial in the long run for individuals who may eventually need help with prescription drugs costs.

Benefiting From All Parts of Medicare

Every Individual who is eligible to receive Medicare can start truly benefiting from all parts of Medicare whether they know it or not.

- Part A can protect individuals from running into problems trying to pay for hospital bills that could really add up if an individual has to stay in a hospital for a prolonged amount of time.

- Part B helps individuals who want to continue to get checkups and doctor visits to make sure they do not have to be bedridden for an extended period of the time if ailments are found that may need to be treated. This plan really helps cut the cost of these simple doctor visits without Part B medical costs could be significantly high.

- Medicare Advantage or Part C is an amazing plan that utilizes all of the plans into one big super plan where individuals can receive all Medicare Plans with just one insurance provider that has limits as to how much they can charge individuals.

- Medicare prescription drug benefit is very important for individuals who have or may get conditions they may require prescription drugs for an extended period of time.

Furthermore, individuals eligible can begin benefiting from all parts of Medicare when they choose to do so with the knowledge that has been provided here.

Deciding Where to Start for Medicare

When deciding where to start for Medicare individuals should start researching or reading articles like these in their early 60s so that they are fully educated before they turn 65 in order for them to not run into any future problems when they become eligible for Medicare.

Enrollment Period

They should first understand the initial enrollment period which begins 3 months before they turn 65 and ends 3 months after an individual turns 65. Next, it would be very beneficial to start visiting a current doctor to see if they have a condition or are likely to have conditions so they can truly know which plans they should utilize.

Be Wary of Medicare Advantage Plans

Another great thing to remember when deciding where to start for Medicare is to watch out for Medicare Advantage plans. Medicare Advantage plans are great because an individual can receive all of the Medicare benefits in one big plan. They are great but individuals must remember that there are limits to these plans since they are offered by health care providers rather than the United States Government. This can cause problems as individuals must only use their plan in certain areas or at certain hospitals which can limit their care, especially if they are planning on moving in the future. These are some very important things to remember and a lot of information has been shared in this article so individuals should make sure they re-read this article and or do further research on Medicare.