The “Must-Know” Facts About the Medicare Enrollment Period

Important Facts About Medicare Open Enrollment

How Does Medicare Open Enrollment Work Going Into 2019? You can enroll in Medicare Part A at 65, but you need to know the procedure for this. Someone who is completely new to the process might not realize all the things that go into this plan, and the only way to make effective changes is to learn about the open enrollment period. You can ask questions like, “when does open enrollment end,” but you also need to know how long that period lasts in the first place. You need to know the same thing about provisional enrollment, and you need to see if there is something you can do to apply after enrollment period or when you turn 65 if that is not during this part of the year.

When Does Open Enrollment End?

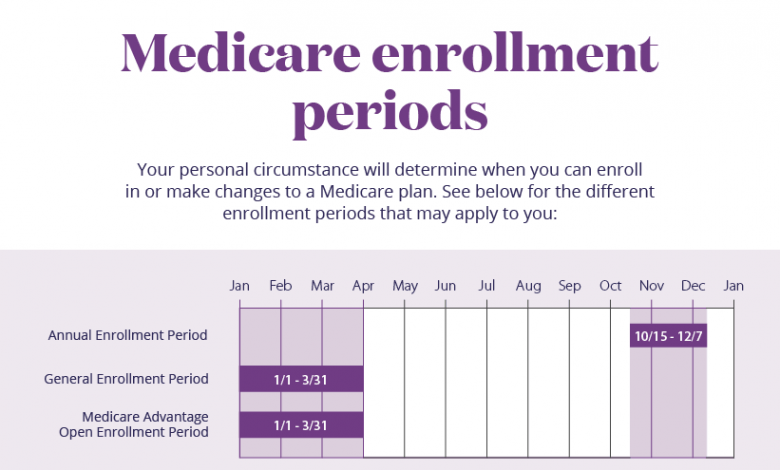

You might start out this process asking, “when does open enrollment end?” or “How long is open enrollment”. This is a fair train of thought because you might research until the last day of the open enrollment period trying to figure out what to do. The only thing that you can do is start researching now because open enrollment ends on December 7th, 2018. There is a period after that where you can apply, but all the normal options will be open until that window closes. You can do it online, or you can call the customer service center to get them to help you with this issue. You might also want to compare insurance plans yourself because that will give you all the information you need to make an educated choice.

Can I Apply After Enrollment Period?

It is a scary question to consider because you might think that you have missed out for the year. This is not the case because there is a provisional enrollment period. These insurance companies are always open for business because they have to find a way to get people onto their rolls when they turn 65 in the middle of the year. There are a lot of people that will go on Medicare at random times because they have retired at a random time, and there are others who will get out of the military and go from Tricare to Medicare. You will have people who have been using a private insurance company because they needed a certain level of coverage, but that is not the case anymore because they want to go to the traditional Medicare coverage. You simply need to contact the national call center to see what they can do for you.

Do I Automatically Enroll In Medicare Part A At Age 65?

You do not automatically enroll in Medicare Part A at 65. You have to be sure that you have enrolled during the open enrollment period, or you could learn about how the enrollment works if you are making this change at an odd time. You can get into the Medicare Part A plan at any time because you are 65, but you are not thrown into the mix unless you ask to get into the Medicare insurance plans. You need to be sure that you know what you are choosing because you have many insurance plans that could be used to help you maintain your health.

Does Everyone Have To Be On Medicare At 65?

You do not have to be on Medicare at 65, and you need to be sure that you have figured out what would work for you when you want to change. You can keep the insurance that you have at 65 because you are already happy with it, and you will start to enjoy the plans that you have changed to when you think it is time to move to Medicare. Some people will retire in the middle of the year, and they can go right into Medicare. Other people will go to Medicare when they lose their insurance, and there are military service members who will want to change from Tricare to Medicare because they think it is time.

How Long Is Open Enrollment?

“How long is open enrollment,” is a common question because you have been wondering what you need to do to get into the program. You can choose to use the enrollment period as a time of research, and you can choose to use the open enrollment period as a time to talk to different insurance companies about what they do. Someone who is trying to make the best decision needs to remember that they are going to choose the Parts A, B, C, and D. You need to get all the plans that match up with your needs and have looked into which plans you actually need.

What Is The Provisional Enrollment Period?

Be sure that you have chosen the plans with help from an associate because they are the people that help you during the provisional period. The period that you get to enroll after the open enrollment might be missing some health plans because they do fill up. There are a lot of other people who are going to have a problem with the health plans they can choose from because they missed out, but you can get what you need most of the time.

What If I Do Not Like The Plan I Chose?

If you dislike the plan that you have chosen, and you need to be sure that you have contacted Medicare to see if you can shift your plan to something else. This could be possible if you have issues with anything from Part A, B, C, or D. You also need to be sure that you have asked about specific plans that might work better for you. Let the customer service associate know what you need out of a plan, and they will make that change for you. This is a very simple decision to make, but you have to actually talk to someone first so that you do not get another bad plan.

Can I Change My Mind?

You can change your mind at any time, and you must contact the call center once again to let them know that you need to make changes to your plan. You must let them know that you have concerns about your plan, and you should ask for an application to change your plan. You can change everything from Plans A, B, C, and D. Some people will simply change their mind when the next open enrollment period comes around, but you need to be sure that you have researched all the plans you could get before making your decision.

How Many Parts Of Medicare Are There?

There are four parts of Medicare that you must be concerned with. Part A will cover your major medical services. You can do most things through Part A, and you will go into Part A before you do anything else when you sign up. The purpose of Part A is to give you traditional insurance, and it is offered through many companies that are part of the Medicare family. You also get to have Part B that will help pay for equipment and other things that are helpful if you need home care. You could get a scooter or a hospital bed from Part B, and you will find that Part B can help you with transportation. This includes:

- Ambulance trips

- Shuttle service to medical facilities

- Life flight

- Transportation to new facilities

Part C is the Advantage plan that people will use when they are looking at ways that they can use a monthly fee-based plan to get medical service. Medicare Part C is not for everyone, but it can help you when you would prefer to pay by the month because you only have a couple of services that you use. Whereas Part D is the prescription plan, and it will help you with all prescription meds including:

- Tiered drugs of all prices. You can read the list of medications and how much they are covered. This is important if you take specific medications.

- IV medications that are used in the hospital or at home

- Special breathing machines that are used to help you and are not covered under Part B

Do You Need Supplemental Insurance?

You need supplemental insurance if you have problems with how much you have spent on certain medical options. You could use the supplemental insurance to cover up all the problems that you are dealing with when you get bills for responsibility. Someone who is trying to make the best financial decisions for themselves need to be sure that they can get a supplemental plan that will automatically kick in. This also means that you will never pay for medical care, and you pay a tiny premium every month for this coverage.